Client

Executive summary

In June, the trend of PTA fluctuated within a narrow range. The market was mainly speculative for spot shortage. From the basis of the basis difference and the near-term monthly price difference, the spot was stronger than the futures in June, and the recent month was stronger than the distant month. The planned equipment overhaul combined with the expected external equipment failure made the supply lacking the increase in volume in June, superimposed the demand for the downstream polyester products, and the PTA social inventory continued to fall. In July, with the resumption of inspection and maintenance equipment, the supply pressure will be alleviated. At present, the processing rebound is significant. The ACP in July is about 775 US dollars/ton. The cost is not high, which is conducive to the continuation of the current processing. Production, there are some devices that have been running continuously for more than one year. The profit is good for the maintenance of this part of the device. However, the demand for polyester and non-polyester is still more than supply, and the spot tension will continue.

In terms of operational recommendations, the recent trading volume and positions of the PTA futures market have declined. The main hype is still mainly short-term, and the unilateral rise is mainly affected by the commodity market atmosphere. Under the tight supply, the long-term curve and the rising water structure make the main force lack the power to make futures. On one side, the increase rate is more limited, and it can be dirated at the bargain-hunting. In terms of the near-month and long-term price difference, the spot price is narrowing, and the main short position shifts the long-term position to promote the narrowing of the price difference. It can continue to operate the nine-in-one counter-sleeve along the downward channel band, and still need to guard against oil prices and commodity markets. The atmosphere changes. for reference only.

1, PTA

1.1 Production and inventory aspects

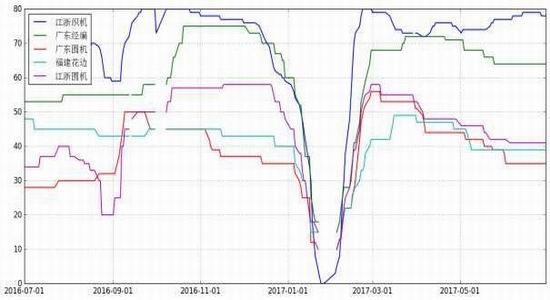

In June, the load on the PTA plant fell slightly. At the beginning of the month, the equipment of Yangzi Petrochemical, Zhejiang Liwan and Yisheng Petrochemical was overhauled, and the load dropped to about 69%. Then BP Petrochemical, Tianjin Petrochemical and Hanbang Petrochemical took turns to overhaul, and the load dropped again. Unexpected failure of Hengli Petrochemical reduced the load to a new low of three months, about 62%. For the whole month, the average monthly load in June was around 70%, a decrease of nearly 2% from the previous month, and the monthly output was about 2.7 million tons.

In terms of PTA demand, in terms of polyester plants, the monthly load of the polyester plant is about 87%, which is basically the same as the average. The polyester output is about 3.35 million tons, corresponding to the PTA demand of 2.85 million tons, plus PTA. Exports and the consumption of PTA in other areas, in June, PTA anti-seasonal continued to destocking, social inventory of about 150,000 tons to 200,000 tons of decline. In July, in terms of PTA supply, in July, there were continuation of maintenance of Hengli Petrochemical, BP Petrochemical, and Hanbang Petrochemical, as well as equipment maintenance of Fujian Jialong. The potential equipment maintenance was 2 million tons of equipment in Yisheng (Ningbo). On the whole, considering the possibility of unexpected equipment failure, it is expected that the PTA load in July will remain around 71%-72%, and the output will be around 275-2.8 million tons. On the demand side, the current downstream products are characterized by structural differentiation, FDY and POY cash flow is better, inventory is lower than the same period of the previous year, while DTY is relatively poor, and inventory is high. Loom load is currently weakly weak, mainly concentrated in water jet loom that is environmentally rectified. The bombing factory is also affected by the bad performance. The rest of the link has not had much impact, and the current polyester load is around 88%. The PTA load is estimated at 72%. The corresponding polyester load is about 85% after conversion. If the demand in the non-polyester field is considered, the supply and demand balance of polyester load is about 81%.

Table 1: List of recent device changes

Source: CCF, Xingzhen Futures R&D Department

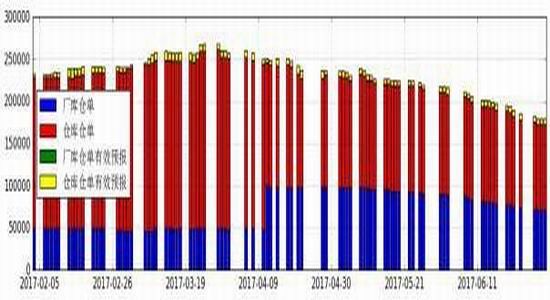

Figure 1: The shortage of spot goods, the warehouse receipts continue to flow out

Source: Zhengshang Institute, Xingzhen Futures R&D Department

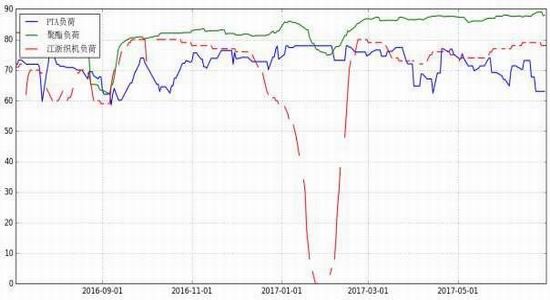

Figure 2: PTA load drop is obvious, polyester load is slightly lowered, and Jiangsu and Zhejiang weaving machines are slightly lowered.

Source: CCF, Xingzhen Futures R&D Department

1.2 Corporate profits

In June, PTA shocked up. The average monthly price of PTA spot was 4,722 yuan/ton, down 19 yuan/ton from the previous month. The average monthly price of CFR China/Taiwan PX spot was 790 US dollars/ton, down by 25 US dollars/ton from the previous month. In June, ACP failed to talk about it. PTA processing is calculated monthly, and the current purchase is now around 435 yuan / ton, rebounding about 70 yuan / ton, a slight improvement.

In July, in terms of PTA cost, ACP talked about 775 US dollars / ton, the previous PX fell with oil prices, the average price fluctuated between 760-790 US dollars / ton. After the destocking action from March to June, PTA's current social inventory remained at a low level, and the futures warehouse receipts continued to flow out. The price increased due to strong demand, and the recent processing gap has risen to around 600 yuan/ton. It is estimated that the PTA social inventory will remain at a low level in July, and the spot price may remain firm, which will facilitate the expansion of processing and promote the increase of load. In addition, major manufacturers will lock in part of the cost due to ACP negotiations, which is beneficial to mainstream manufacturers. Increase supply and ease spot pressure.

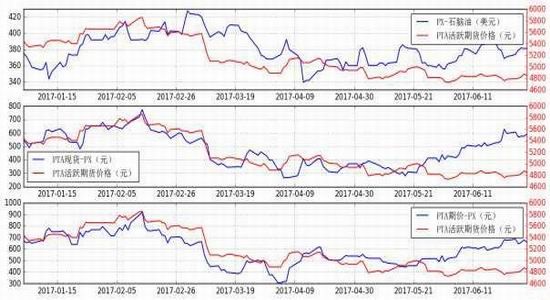

Figure 3: The crack spread remains low, and the PTA processing is poorly picked up due to the PX fall.

Source: WIND, Xingzhen Futures R&D Department

Figure 4: The basis is continuously narrowed

Source: WIND, Xingzhen Futures R&D Department

2, PTA downstream - polyester factory

In June, the price of polyester products showed structural differentiation, FDY rose more, DTY performed poorly, and the rest remained more volatile. The polyester factory inventory also showed significant differentiation, FDY and POY decreased more, and DTY only decreased slightly. In the production and sales of polyester, June was slightly better than that in May, and the demand for terminal speculative stocking occasionally appeared.

In terms of polyester chips, the price fluctuated in June. In terms of monthly average price, the semi-light slice was at 6652 yuan/ton, and the light slice was at 6842 yuan/ton, up by 100 yuan/ton.

For polyester filaments, as of the end of the month, POY150D/48F, FDY150D/96F and DTY150D/48F were respectively at 7,850 yuan/ton, 8565 yuan/ton and 9,470 yuan/ton, and FDY rose more at 500 yuan/ton, with an average monthly increase of 400 yuan. About RMB/ton, POY and DTY have an increase of about 200 yuan/ton, and the average monthly increase is about 80 yuan/ton.

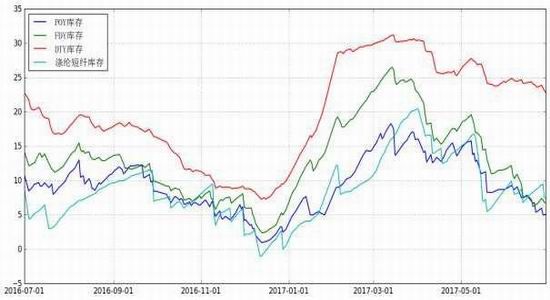

In the inventory of polyester filament yarn, it continued to destock in June. As of the end of the month, the stocks of POY, FDY and DTY in Jiangsu and Zhejiang were 5.1 days, 6.8 days and 22.8 days respectively, down by 3 days, 5 days and 1 day, respectively. POY, FDY, and DTY stocks were 7.19 days, 8.5 days, and 24 days, respectively, with a 4-5 day drop in the chain.

In July, from the perspective of terminal stocking, the total stock of terminal raw materials ranged from 7 to 20 days, mostly in January-February. In the sales of grey cloths, the overall atmosphere is still good, and the price of grey cloths has been followed up, but it has not been lost. Future grey fabric prices will affect terminal stocking needs. Whether the price of DTY can go up will affect the production of polyester plants. At present, DTY stocks are sufficient, and the raw materials may fluctuate in a narrow range, and the price increase may be low. On the contrary, the FDY inventory is low, the price may continue to rise, and the processing difference is good, stimulating the polyester plant to continue to maintain high load operation.

Figure 5: POY, FDY, DTY processing is moderately picking up

Source: WIND, Xingzhen Futures R&D Department

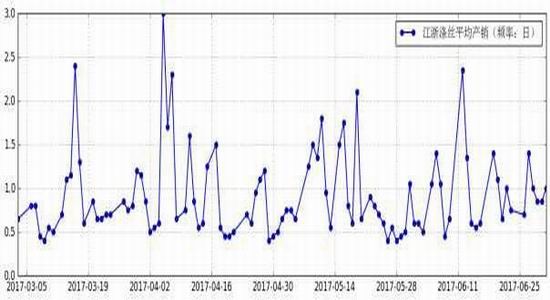

Figure 6: Jiangsu and Zhejiang filament production and sales - the overall general, there is significant volume in the middle of the month

Source: CCF, Xingzhen Futures R&D Department

Figure 7: Inventories of polyester products in Jiangsu and Zhejiang markets - continued to decline

Source: CCF, Xingzhen Futures R&D Department

3. PTA downstream - textile terminal

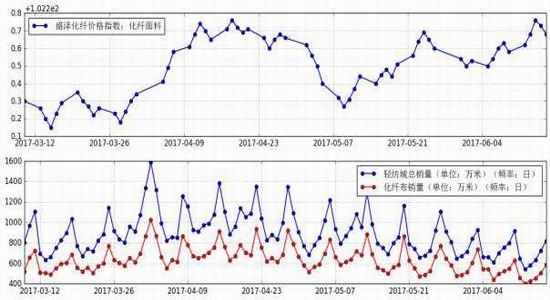

In June, all textile bases continued to maintain high-load operation. As of the end of the month, the load of Jiangsu and Zhejiang looms, Jiangsu-Zhejiang, and South China looms were 85%, 78%, and 55%, respectively.

According to the data of China Textile City, the sales volume of the grey cloth market continued to fall in June. The total transaction volume of China Textile City in June was about 7.06 million meters per day, which was about 1.6 million meters per day, and the sales of chemical fiber cloth was 5.12 million meters per day. Left and right, the chain fell by about 1 million meters / day. From the perspective of changes in the month, the U-shaped trend is presented, the first is better than the late, and the second is better than the middle.

Figure 8: Shengze fabric index is significantly lower, textile city volume is gradually decreasing

Source: WIND, CCF, Xingzhen Futures R&D Department

Figure 9: Textile machinery load everywhere

Source: CCF, Xingzhen Futures R&D Department

4. Linkage between PTA and other varieties

The crude oil market fell sharply in June.

At the beginning of the month, although the EIA showed that US crude oil inventories fell more than expected, the resumption of production in Libya's Sharara field caused the market to worry about the increase in crude oil supply. Libya and Nigeria were both OPEC production exemptions. In addition, the continuous increase in the number of drilling and production in the United States has aggravated market concerns. The break-up between Saudi Arabia, Egypt, the United Arab Emirates and Bahrain and Qatar triggered market concerns about geopolitical risks, and oil prices were boosted in the short term. And then EIA showed that the surge in inventory once again suppressed the price of oil.

In the middle of the month, the news showed that there were problems in the oil pipelines in Libya and Nigeria, indicating that the crude oil production in Nigeria and Libya was not stable, and the market worried about cooling down. However, the increase in US oil product inventory and drilling again weakened the rebound of oil prices, and the oil price reached 7 The monthly low, after which the market’s concerns about supply continue to weigh on oil prices.

At the end of the month, the news showed that China's refining activities are declining, which has aggravated the market's worries about global oversupply. At the same time, the increase in production in Libya and Nigeria has once again suppressed oil prices. The oil price hit a low of nearly 10 months. After the speculative fund appeared to buy on dips, coupled with the latest EIA inventory and drilling well, the oil price rebounded six consecutive years.

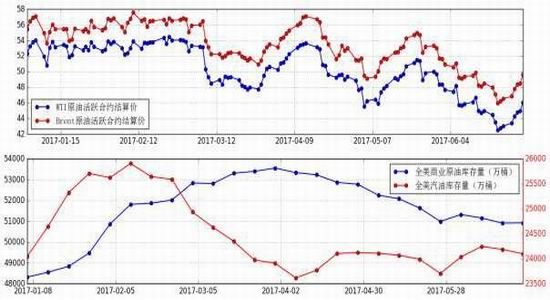

Figure 10: National gasoline inventories fell significantly, crude oil inventories still slowly increased

Source: WIND, Xingzhen Futures R&D Department

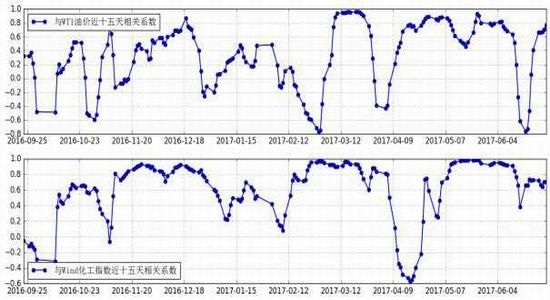

Figure 11: Correlation coefficient between TA period price and WTI oil price and WIND chemical index for nearly 15 days

Source: WIND, Xingzhen Futures R&D Department

5, operational recommendations

In June, the trend of PTA fluctuated within a narrow range. The market was mainly speculative for spot shortage. From the basis of the basis difference and the near-term monthly price difference, the spot was stronger than the futures in June, and the recent month was stronger than the distant month. The planned equipment overhaul combined with the expected external equipment failure made the supply lacking the increase in volume in June, superimposed the demand for the downstream polyester products, and the PTA social inventory continued to fall. In July, with the resumption of inspection and maintenance equipment, the supply pressure will be alleviated. At present, the processing rebound is significant. The ACP in July is about 775 US dollars/ton. The cost is not high, which is conducive to the continuation of the current processing. Production, there are some devices that have been running continuously for more than one year. The profit is good for the maintenance of this part of the device. However, the demand for polyester and non-polyester is still more than supply, and the spot tension will continue.

In terms of operational recommendations, the recent trading volume and positions of the PTA futures market have declined. The main hype is still mainly short-term, and the unilateral rise is mainly affected by the commodity market atmosphere. Under the tight supply, the long-term curve and the rising water structure make the main force lack the power to make futures. On one side, the increase rate is more limited, and it can be dirated at the bargain-hunting. In terms of the near-month price difference, the spot price is narrowing under the tension of the spot, and the main short-selling positions have also moved the distant month to promote the narrowing of the price difference. It can continue to buy nine throws along the upward channel band operation, and still need to be wary of oil prices and commodity market atmosphere. Variety. for reference only.

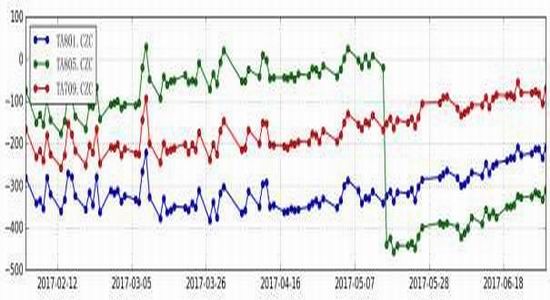

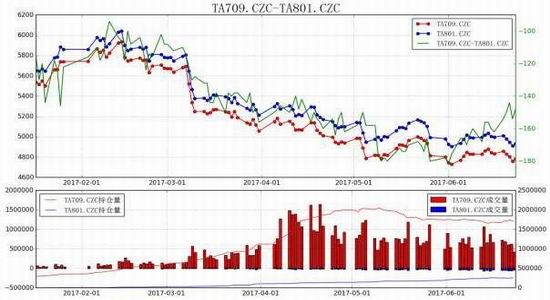

Figure 12: TA1709 Day K Line Chart

Source: WIND, Xingzhen Futures R&D Department

Figure 13: TA1709 net position change

Source: WIND, Xingzhen Futures R&D Department

Figure 14: TA1801 net position change

Source: WIND, Xingzhen Futures R&D Department

Xingzhen Futures Liu Zheng

Sina statement: Sina's posting of this article for the purpose of transmitting more information does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.Rubber Bushings, usually called Rubber Sleeve Bearing, Rubber Sway Bar Bearing, Rubber Damper,Rubber Flange Bearing, Rubber Plain Bearing,etc, is a fixed or removable cylindrical lining used to constrain, guide, or reduce friction toprotect an inside surface, which is known as an insulating lining for a hole through which a conductor passes and an adapter threaded to permit joining of pipes with different diameters.often with screws.

Custom Rubber Bushing,Rubber Energy Bushing,Bushing For Auto Parts,Parts Suspension Bushing

Xiamen The Answers Trade Co.,Ltd. , https://www.xmanswerssilicone.com